The advantages of unit-linked policies

Interview : João Espanha, lawyer

Expert's word: Three questions to João Espanha – Founding partner - Espanha e Associados, Lisbon - Portugal

"According to me, the advantages are essentially great flexibility and security"

João Espanha explains in which cases he recommends taking out a unit-linked life insurance policy and why choose Luxembourg specifically.

Text version of the interview:

What are the advantages of a unit-linked life insurance contract?

According to me, the advantages are essentially great flexibility and security. In other words, it is possible for an investor to carry out, through a unit-linked insurance contract, various investment strategies of his/her choice, in the medium to long term, in accordance of course, with the terms of the contract. This combined with the security of having these savings within an insurance company and not in “complete freedom”. It seems to me that these are the main advantages, in general, of a unit-linked life insurance policy.

What are the types of scenarios for which you would recommend a unit-linked life insurance contract?

I would recommend it especially in cases where the investors have medium-to-long-term saving objectives, mainly for two reasons: the flexibility issue, which I have already mentioned; it is possible for the savers to pursue different investment strategies, as they wish, while the contract is effective. And, on the other hand, for having taxation linked to this type of contracts which is, in the Portuguese case, long-standing and stable, and thus, offers a premium to such savers, in the medium-to-long-term term, as long as, under their portfolio, they finally invest their savings within a unit-linked life insurance contract.

Why choose Luxembourg as a place to subscribe a unit-linked life insurance contract?

I would essentially name two reasons: on one hand, the professionalism associated with the market. Luxembourg is a jurisdiction known for having the financial sector as its essence and, therefore, we have managed to find good professionals, good companies and good regulation. On the other hand, mainly because of the security issue, with the so famous Luxembourg’s triangle of security, which involves a very active and vigilant regulation of the insurance activity, policyholders benefit from a credit privilege, that is, in case of a default, they are always the first to recover the assets, their specific assets. Finally the portfolio is deposited in a bank outside the scope of the insurance company, which is also regulated, controlled and it is therefore difficult to find a more secure place than Luxembourg.

Unit-linked versus euro funds

The advantages of unit-linked policies

Statistics on Unit-Linked Policies

The various available investment vehicles

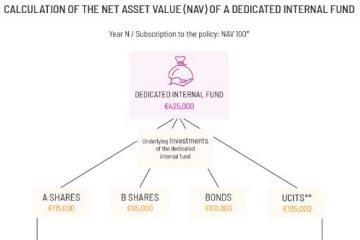

Calculation of the NAV of an internal dedicated fund

The Luxembourg unit-linked life insurance policy benefits from great flexibility and security. In addition, it allows policyholders to diversify their assets by opting for personalised management strategies according to their risk profile. This combination of flexibility and security makes the Luxembourg life insurance policy an essential wealth management tool.