The Specialised Insurance Fund: a Luxembourg innovation in investment vehicles.

Definitions and particularities of the SIF

The definition of a Specialised Insurance Fund is short and simple; it is: “an internal fund, other than an internal dedicated fund, with or without direct lines but not including a performance guarantee, which serves as the investment vehicle for a single policy.2"

Specialised Insurance Funds are therefore defined from the outset as being different from internal dedicated funds which are "managed by a single manager3". In fact, this is not the only difference since investments in Specialised Insurance Funds may be made without any conditions as to premium or wealth, unlike the internal dedicated fund (IDF) which requires a minimum investment of EUR 125,000.

The SIF does not have the advantage of the exemptions granted to IDFs for family funds, often referred to as "umbrella" dedicated funds4.

Although the subscriber to several policies is only able to invest in one single dedicated fund, the Specialised Insurance Fund may only act as the investment vehicle for a single policy. As Karine Vilret, our understanding of the text of the circular letter is that an insurance policy may be backed by several Specialised Insurance Funds. We will see, later, that the different types of SIF which result from insurers' practices render this hypothesis meaningful.

Assets eligible for Specialised Insurance Funds

"The investment limits for a given asset are determined by applying the limits in Annex 1, and depend on the category of the client as defined in point 2. These limits apply, by reference, to the overall value of the policy.7"

As regards eligible assets, the legislature did not differentiate between SIFs, and other IDF or ICF investment vehicles. Thus, all the assets listed in Annex 1 of the CAA’s Circular Letter 15/3 are theoretically eligible in a Specialised Insurance Fund within the limits imposed by the subscriber's classification.

If an SIF coexists with and one or more IDFs, the manager of the IDF must be informed about the composition of the SIF in order to avoid any unintended concentration.

The insurer remains free to establish a more restrictive list of assets based on its internal policy, on its technical capacity to receive orders for securities or on the legislation of the country in which the contract is marketed. We are thinking particularly of France or the United Kingdom.

Additional points of difference between Specialised Insurance Funds and Internal Dedicated or Internal Collective Funds: the assets which constitute the technical [insurance] reserve need not be deposited in a specific account or sub-account for each fund but may, however, be deposited with different custodian banks.

Major characteristic of Specialised Insurance Funds: the choice of assets by the subscriber

"Each of the specialised insurance fund’s assets is chosen directly by policyholders, either when initial or subsequent premiums are invested, or during a switch.8"

The assets of the Specialised Insurance Fund are chosen by the subscriber of the “policy, who remains the sole decision-maker in the choice of assets9", who "directly participates in the choice of the assets of the SIF10", and who therefore cannot “transfer to the insurer or to a third party the power to select the assets on his behalf11".

Circular letter 15/3 therefore offers subscribers freedom of choice. However, the novelty of the Specialised Insurance Fund, a lack of perspective, or the absence of case law are sufficient reasons to encourage insurers to plead in favour of assisting the subscriber. For example, some insurers do not systematically ask the policyholder to engage an advisor, but others do. The advisor may sometimes be the insurer itself, or an external professional party, who will provide the subscriber with its expertise.

Is an order given to the custodian bank a switching transaction or an investment transaction?

The practical arrangements for executing the subscriber's choices when the initial or subsequent premiums are invested or when switches are made enable insurance companies to differentiate themselves from each other.

While some insurance companies have made preparations for accepting and executing the subscribers' choices, as banks do, others prefer that these transactions be executed by a professional third party.

Some companies consider that insurance brokers are qualified to place orders for the shares, bonds, UCITS12 and other assets which constitute a Specialised Insurance Fund. “Placing an order" is therefore a switching transaction13 which the broker executes in his capacity as agent of the subscriber of a policy backed by an SIF.

Others consider that replacing one financial asset with another within the same SIF may only be executed by a professional who, in compliance with the legislation of his home country, has the approvals required for the financial instruments selected by the subscriber. In the particular case of France, a conseiller en investissement financier (financial investment advisor, or CIF) appointed by the subscriber and approved both by the insurance company and the custodian bank, may submit orders for switching between UCITS funds.

The way in which a company classifies the transaction will determine the method used to execute it and the choice of the investor’s legal position.

It is therefore not impossible for one company to consider that a broker may execute a switching transaction between two UCITS funds and for another, acting in its capacity as a CIF, to consider that the same person may execute this investment transaction within the Specialised Insurance Fund.

Another sign of the uncertainty surrounding the Specialised Insurance Fund is that some companies will limit the number of switches made by the subscriber.

Different types of Specialised Insurance Fund

Circular letter 15/3 of the Luxembourg Insurance Commissioner (the CAA) specifies only one Specialised Insurance Fund, but two main families of SIFs have quickly emerged: the Buy & Hold SIF and the Advisory SIF15.

The internal dedicated fund, with its discretionary management, did not meet the needs of some subscribers or the technical constraints of some asset managers.

In particular, the dedicated fund did not allow for a Buy & Hold type of management which required that listed or unlisted securities (shares, bonds, funds, etc.) be held for long periods or until maturity of the securities. Nor did the dedicated fund make it possible to accommodate an Advisory mandate in which the financial institution offers its client investment or switching transactions on the financial products. The fact that the financial institution's client systematically validates the proposal significantly limits the extent of the professional’s responsibility. Buy & Hold and Advisory SIFs have made it possible to include these two types of management in insurance policies.

In addition, the Specialised Insurance Fund enables banks and asset managers to "clean up the discretionary management" which naturally applies in dedicated funds, and to remove positions for which there are restrictions on sale.

The advantage of the Specialised Insurance Fund when managing external funds

The Specialised Insurance Fund has brought real flexibility to life insurance policies by enabling subscribers to choose their policy’s assets and thus to align the management of their policy as closely as possible with their objectives and needs.

Subscribers have access to the same investment universe in an SIF as the universe to which they would have had access through discretionary management in an IDF. Thus, they have a much wider freedom of choice of these assets than they have when managing his policy with external funds. Indeed, insurance companies generally offer a relatively limited list of a few hundred external funds (uniquely UCITSs) from which subscribers must make an investment choice. Within an SIF, subscribers have access to all the assets permitted by their category and, in particular, are able actively to manage their investments.

The management of switching between different assets is also quicker and more flexible in an SIF, since the orders are passed by clients, or their advisors, to the RTO16 agent who executes them on their behalf. In the case of investment in external funds, changes of investment vehicles require a “switching” in the insurance sense, which entails more cumbersome administrative management than transactions within the SIF.

Conclusion

Even though the development of the first policies backed by Specialised Insurance Funds took time and the practical arrangements may seem complex or be differently interpreted by different insurance companies, it is undeniable that the Specialised Insurance Fund has found its place in the range of wealth management tools offered by Luxembourg insurance companies.

Not only does it supplement and clarify the existing offer - particularly the offer of internal dedicated funds - but more importantly it meets the needs of subscribers, which have so far remained unanswered, and also offers solutions to the financial sector, particularly to banks and asset managers. There is no doubt that the Specialised Insurance Fund is an innovation which will help strengthen the uniqueness of Luxembourg insurance companies.

1 Amended by Circular Letter 19/2 of 15 January 2019 (coordinated version - http://www.caa.lu/uploads/documents/files/circ19_2.pdf).

2 Article 1(j) of Circular 15/3 of 24 March 2015 from the Luxembourg Insurance Commissioner (CAA).

3 Article 1(i) of Circular 15/3 from the CAA.

4 Article 5.3.1 of Circular 15/3 from the CAA. In exceptional cases, the CAA may approve the linking of several policies, subscribed by the same policyholder or by several policyholders united by marriage or close family ties, to one single dedicated fund. Remember that internal collective funds of types A, B, C and D which are reserved for a closed circle of subscribers, make it possible to achieve a fairly similar result.

5 Idem

6 Karine Vilret, Droit de l'assurance-vie au Luxembourg (Life Insurance Law in Luxembourg), Promoculture Larcier, 2018, p.236.

7 Article 5.4 of the CAA’s Circular Letter 15/3.

8 Article 5.4 of the CAA’s Circular Letter 15/3.

9 Karine Vilret, Droit de l'assurance-vie au Luxembourg (Life Insurance Law in Luxembourg), Promoculture Larcier, 2018, p.239.

10 Idem

11 Idem

12 UCITSs: Undertakings for Collective Investment in Transferable Securities.

13 There is no definition of “switching” in insurance but please see Karine Vilret, Droit de l'assurance-vie au Luxembourg (Life Insurance Law in Luxembourg), Promoculture Larcier, 2018, p. 244 et seq.

14 Buy & Hold is a passive investment strategy which involves choosing investments carefully and holding them for the long term.

15 Advisory is a strategy which enables the subscriber to manage his portfolio himself, whilst also being advised or assisted.

16 Receipt and Transmission of Orders.

Born of the imagination of the Luxembourg legislator, the fonds d’assurance spécialisé (Specialised Insurance Fund, or SIF) appeared with Circular Letter 15/3 issued by the Commissariat aux Assurances (the Luxembourg Insurance Commissioner, or CAA) on 24 March 20151. This is by far the most significant innovation in insurance in recent years and is proof of the dynamism of this sector in Luxembourg.

The Specialised Insurance Fund complements the range of different categories of investment vehicles available for unit-linked policies, alongside other internal, dedicated and collective funds, as well as external funds.

Unit-linked versus euro funds

The advantages of unit-linked policies

Statistics on Unit-Linked Policies

The various available investment vehicles

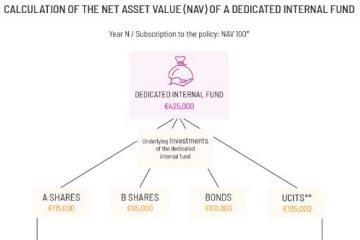

Calculation of the NAV of an internal dedicated fund

The specialised insurance fund is an eligible fund within Luxembourg life insurance contracts depending on the subscriber's country of residence. The distinctive feature of the specialised insurance fund is that it serves as a vehicle for a single contract for which the policyholder is free to choose the underlying assets in accordance with regulation 15/3 of the Commissariat aux Assurances.