Unit-linked policies

Unit-linked versus euro funds

The advantages of unit-linked policies

Statistics on Unit-Linked Policies

The various available investment vehicles

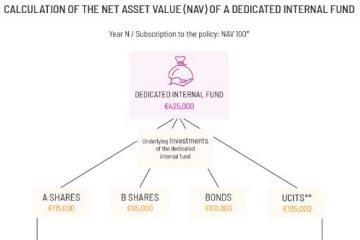

Calculation of the NAV of an internal dedicated fund

Discover the flexibility offered by unit-linked policies.

There are different types of life insurance policies such as policies in EUR or unit-linked policies. The latter ones enable you to invest in a variety of financial instruments: equities, bonds, UCITS (undertakings for collective investment in transferable securities), etc.

Unit-linked life insurance policies are flexible: they can be tailored to the subscriber's situation, objectives and investment horizon.

They are sustainable tools for managing your savings, to be used as part of an overall wealth management strategy.

Unit-linked life insurance policies are one of the most important advantages of Luxembourg's wealth management offer.

Specific features

In a unit-linked life insurance policy, the risk is borne by the subscriber and the value of the policy increases or decreases in accordance with changes in the financial markets.

A unit-linked life insurance policy is expressed in terms of the number of its units, which are classified according to their asset classes (e.g. equities, bonds, real estate, etc.), their geographic area (United States, Europe, emerging countries, etc.) and their investment sectors (health, infrastructure, technology, etc.)

Depending on the sums to be invested, the subscriber has access to quite a broad spectrum of assets, as set out in Circular 15/3 from the Commissariat aux Assurances.

The investment vehicles available in unit-linked policies

There are two main categories of investment vehicles available in unit-linked policies:

Internal funds, which are themselves broken down into three categories:

- Internal Collective Funds (ICF): internal to the insurance company, they group together several subscribers.

- Internal Dedicated Funds (IDF): managed by a single manager, they are generally used as investment vehicles for individual policies.

- Specialised Insurance Funds (SIF): these are internal funds which serve as the investment vehicle for only one policy, in which the subscriber plays a full part in the management of the assets.

External funds: these are undertakings for collective investment (UCIs or unit trusts) established outside the insurance company, managed by asset managers, and subject to approval and continuous prudential supervision by a country’s supervisory authority. They may be UCITS, funds of hedge funds, or funds of real estate funds.

The different management styles

Depending on his/her investor profile, his/her risk appetite and the investment vehicles held within a unit-linked policy, subscribers will have access to different types of management:

- Subscriber management,

- Profiled management,

- Discretionary management.

If you would like to learn more about unit-linked life insurance policies, please do not hesitate to download the white paper above.

The unit-linked life insurance contract allows to invest in a wide range of investment vehicles. There are two main categories of investment vehicles in a unit-linked life insurance contract. Firstly, external funds, managed by third parties and established outside the insurance company (UCITS, alternative funds or real estate funds). There are also internal funds, devided into three categories: internal collective funds, internal dedicated funds and specialised insurance funds. All three are internal funds within the company. All eligible investments within a unit-linked contract are subject to circular letter 15/3 of the Commissariat aux Assurances.