Why choose a life insurance policy? What are the advantages?

Expert's word: Three questions to Stéphanie Barreira, FBT Avocats S.A. - Paris, Geneva

“A life insurance policy remains the preferred investment for French investors.”

Luxembourg life insurance policies are often used in the connection with international estates. It is particularly suitable for clients wishing to access a range of tailor-made solutions and benefits, in most European countries, from a favourable tax regime.

Text version of the interview:

What do you consider are the advantages of a life insurance policy?

A life insurance policy remains the preferred investment for French savers. A life insurance policy meets a saving objective.

You can make unscheduled contributions, with as much flexibility as you wish, and you may withdraw income if this has been programmed. For example, you may use it to supplement your pension, to meet future needs associated with dependency requirements in later years or, for example, to satisfy an investment-related objective since the assets are invested in a capital accumulation fund.

A life insurance policy also makes it possible to meet the objective of transferring assets to close family members, but also to more distant relations and to third parties. It makes it possible to transfer an asset as securely as possible, and to be flexible and unrestricted in the allocation of the assets at the time of the succession. For this reason, I believe that French savers continue to be interested by life insurance policies.

In which cases would you recommend taking out a life insurance policy?

There are different reasons why we recommend taking out a life insurance policy. We recommend taking one out to reduce tax by minimising the burden of income or property wealth tax; or to reduce the tax burden on transfer duties. Regarding tax income, remember that it is only payable if the saver surrenders all or part of the policy. Provided that the saver is able (and in a position) not to have to withdraw this cash but can keep it invested over the medium to long term, we may consider that he will not suffer any tax over time. As for Property wealth tax, please be aware that life insurance policies unfortunately remain subject to property wealth tax. But this only applies to the taxable portion of the underlying property assets, so that if the subscriber has not invested assets in property funds, we can deliver life insurance policies which will not be subject to property wealth tax.

Finally, regarding the transfer and organisation of a future inheritance, we recommend life insurance policies for customers to make the best preparation of their savings, to get flexibility and freedom of choice. For example, we know that it is possible, thanks to life insurance policies, to make grants to third parties who are not entitled to inherit. These third parties will be able to benefit from an advantageous tax system, from a tax deduction of EUR 152,500 (for example), and from tax which may be limited to 31.25% of the lump sum if the saver invested the premiums before his 70th birthday. Thus, a third party will be able to benefit from these very attractive terms and conditions.

But there is also the opportunity to optimise and transfer capital over several generations, for example by including beneficiary clauses which separate the attributes of ownership, by providing for life-interest ‘usufruct clauses’ in the first instance and for ‘bare ownership clauses’ in the second instance, which makes it possible to transfer capital over two generations.

What are the benefits of taking out a Luxembourg policy?

Well I have to say Luxembourg life insurance policies are very successful in Europe and more particularly in France. They have undeniable advantages and I believe that the first of these is the ‘super privilege’ enjoyed by savers. Indeed, savers concerned with protecting their assets will be attracted by this Luxembourg super privilege. Such savers are considered to be first-ranking creditors because their assets are not placed in the life insurance company's balance sheet but are registered with an independent custodian bank in a segregated account. But this is not the only advantage of these Luxembourg life insurance policies: the variety of assets eligible for Luxembourg life insurance policies is also a significant benefit. These include UCITS funds which may be managed by companies established right around the world. We also have specialised insurance funds called ‘dedicated internal funds’, which are widely used, very common and widely used by Luxembourg life insurance companies.

In addition to these two advantages, I would also add, and would stress, the tax neutrality enabled by Luxembourg. In fact, Luxembourg does not levy a withholding tax on lump sums paid on death or withdrawn by these savers surrendering part of their assets.

Finally, a non-resident will be taxed in his country of residence - where he uses to live; and tax will not be imposed in Luxembourg but only in the country of residence, which is a significant advantage. This avoids the risks of double taxation, which can't be avoided when taking out a French life insurance policy.

Why do you recommend taking out a Luxembourg life insurance policy as part of an international asset management strategy?

We are dealing with an increasingly mobile customer-base, and customers and savers have come to terms, firstly, with this internationalisation of the securities exchanges and, secondly, with their future mobility, so that, while preparing to move their residence outside France, for example, it may be useful to minimise any risk of re-establishing any linkage to residence in France. Please note that the criteria for residence in France are quite numerous and the fact of maintaining a large number of life insurance policies taken out, for example, with French life insurance companies, could be a reasonable indicator which might be used by the French tax authorities to re-establish tax residence in France. Thus, as part of relocation, one should recommend to customers that they take out Luxembourg life insurance policies in order to avoid any risk of a double taxation of re-establishing connections with France.

The advantages of a unit-linked life insurance policy

Why choose a life insurance policy? What are the advantages?

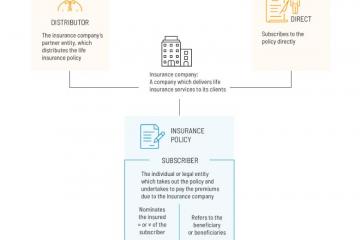

How a life insurance policy works

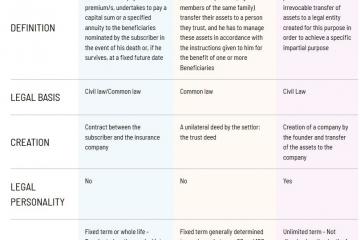

Life insurance policy / Trust / Foundation: the comparative

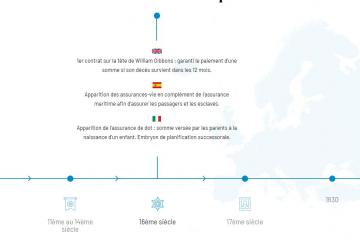

History of life insurance in Europe

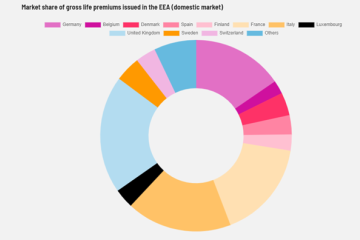

European statistics on life insurance

The Luxembourg life insurance contract is a flexible estate planning tool that allows you to build up savings or a supplementary revenue for pension. It allows you to optimise your estate by giving you more flexibility and freedom, or by passing on your capital over several generations. The Luxembourg life insurance policy also makes it possible to manage mobility issues in the event of a transfer of residence abroad.