Life insurance policy / Trust / Foundation: the comparative

Reading time: 10 min

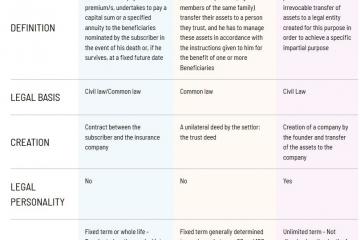

| LIFE INSURANCE POLICY | TRUST | PRIVATE FOUNDATION | |

|---|---|---|---|

| DEFINITION | A contract by which the Insurer, in return for the payment of a premium/s, undertakes to pay a capital sum or a specified annuity to the beneficiaries nominated by the subscriber in the event of his death or, if he survives, at a fixed future date | Arrangement by which one or more related persons (e.g. members of the same family) transfer their assets to a person they trust, and he has to manage these assets in accordance with the instructions given to him for the benefit of one or more Beneficiaries | Arrangement for the permanent and irrevocable transfer of assets to a legal entity created for this purpose in order to achieve a specific impartial purpose |

| LEGAL BASIS | Civil law/Common law | Common law | Civil Law |

| CREATION | Contract between the subscriber and the insurance company | A unilateral deed by the settlor: the trust deed | Creation of a company by the founder and transfer of the assets to the company |

| LEGAL PERSONALITY | No | No | Yes |

| TERM | Fixed term or whole life - Terminated on the survival (at a given age) or the death of the insured, or by the ending of the term, or by total redemption of the policy | Fixed term generally determined to maximum between 80 and 100 years | Unlimited term - Not dissolved on the death of the founder |

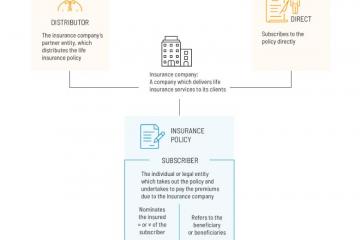

| PARTIES | - Subscriber: the person who takes out the policy - Insured: the person to whom the insured risk relates and whose death or survival triggers payment under the policy - Beneficiary: the person(s) nominated by the subscriber to receive the capital sum at the termination of the policy |

- Settlor: the person who sets up the trust with all or part of his assets - Trustee: the administrator of the trust who has powers of management and allocation over the assets placed in trust - Beneficiary(s): the person(s) to whom the trust’s assets, income, etc. reverts |

- Founder: the person creating the foundation and to which he contributes his assets. - Board: management body of the foundation, composed of several members. - Beneficiary(s): the person(s) who benefit from the foundation (share of income, share of assets, etc.). |

| ASSETS | Depending on the Luxembourg Insurance Commission’s circular, LC15/3 | All types of asset including life insurance policies* | All types of asset including life insurance policies* |

| OWNERSHIP OF ASSETS | Insurance company | Trustee (legal ownership) Beneficiary (equitable owner) |

Foundation |

| MANAGEMENT | Management of the policy conducted in accordance with the investment profile of the client by an authorised manager** | Trustee, depending on the terms of the "trust deed" | Board made up of directors with the objective of accomplishing the task assigned to them (= purpose of the foundation) |

| ADVANTAGES | - Transmission of assets to the beneficiary(s) of its choice thanks to the beneficiary clause - Estate planning - Envelope capitalising to make it profitable and value its capital over time |

- Wealth Preservation - Estate Planning - Preservation of Confidentiality - Asset Protection |

- Preservation and management of assets - Transferral of assets in strict confidentiality - Protection and maintenance of one or more people |

*Subject to acceptance by the Insurance Company

**Except country specificities or underlying assets specificities

This table shows the general characteristics of the different "structures". Each country applies its own legal and tax rules to them. It should be noted that certain "structures" may not be recognised in some countries.

Do you wish to have more information?

Contact us

The contents of this theme

Reading time: > 3 min

The advantages of a unit-linked life insurance policy

Depending on the policyholder's country of residence, the life insurance contract has different characteristics. Discover them in this animated infographic.

Reading time: < 5 min

Why choose a life insurance policy? What are the advantages?

What are the advantages of a life insurance contract? Savings, flexibility, ... The answer in this video interview.

Reading time: < 2 min

How a life insurance policy works

Life insurance contract: how does it work? Explanatory infographic of the functionning of a life insurance contract.

Reading time: 10 min

Life insurance policy / Trust / Foundation: the comparative

What are the differences between a life insurance contract, a trust and a foundation? Detailed characteristics in a comparative table.

Reading time: 5 min

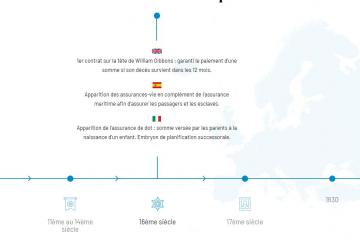

History of life insurance in Europe

A look back at the first life insurance policies that appeared in antiquity through this timeline.

Reading time: 8 min

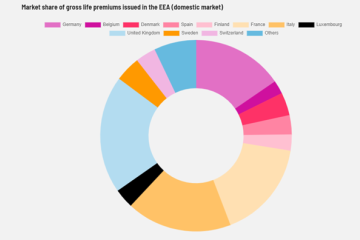

European statistics on life insurance

How much is invested in life insurance policies in Luxembourg?

Life insurance contract, trust or foundation: 10-point comparison.

Life insurance contracts, trusts and foundations have completely different uses. They don't have the same legal basis, the foundation has a legal personality while the life insurance contract and the trust do not. All these elements distinguish these asset management tools.